Employment situation update

Are we seeing a "restorative force" in the labor market data?

As I mentioned in my previous ‘teaser’ post, I’m finally returning to normal after the cross-country move. And just in time for my return to monitoring the models there are some interesting potential — and I must stress potential — phenomena appearing the labor market data.

One thing I noticed in previous updates (e.g. this one from last August where I started using the term “the littlest recession”) is that JOLTS data appeared to be moving towards what would be the extrapolated pre-stimulus / post-pandemic equilibrium. Given measurement noise as well as the uncertainty in estimating the pandemic and stimulus shock (especially given how close they are to each other), this still seems to be true:

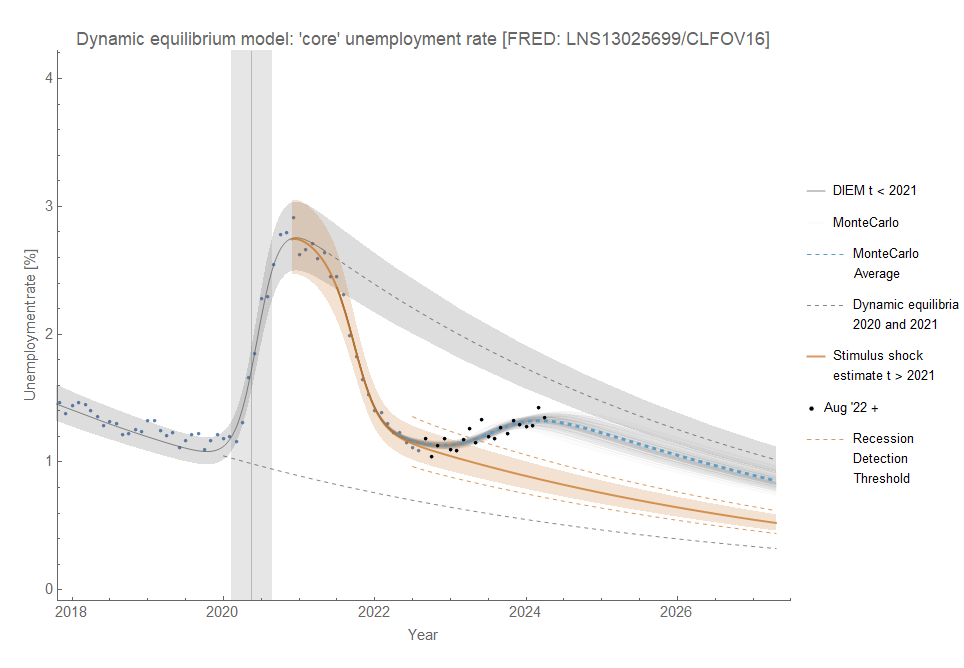

What is interesting is that the (core1) unemployment rate seems to be doing something similar:

The thing is — this is not in the baseline dynamic information equilibrium model (DIEM). The sizes of non-equilibrium shocks do not depend on each other. If we are seeing a “restorative force”, that would mean something new. In the past, I have considered two different hypotheses:

Causal Entropic Forces. A restriction that excludes portions of the volume of the state space.

Step Response. A result of sharp shocks hitting a band-limited system.

There is such a limited amount of data at this point; we only have a few dozen shocks at best to these macroeconomic time series, many of them correlated across series like unemployment and job openings here. It would be hard to distinguish between possibilities. However, as step response usually has over- and under-shooting while causal entropic forces would tend to push the system back to previous equilibria if pushed away there’s at least one way to try to resolve it over the next several decades as more data becomes available.

The other hypothetical effect that isn’t in the baseline DIEM is the noise floor at an initial claims rate2 of approximately 0.15%3 — that seems as plausible an explanation of the lack of signal in initial claims data as ever:

There may be other noise floors in other metrics but I haven’t seen them. There should be one > 0.1% for the unemployment rate4 based simply on the noise in the time series. At a current unemployment level of ~4%, we’re nowhere near close enough to see it.

For the last update graph, we have the prime age employment population ratio, which is continuing to show the dynamic equilibrium trend growth rate at a lower level post-pandemic than the extrapolated pre-pandemic equilibrium. This is one place where there hasn’t been a restorative force — or even a noticeable adverse post-stimulus shock. That creates some complications for any restorative force model, but would be more in line with step response as this measure has almost the entire working population contributing to it (making it more like an over-damped system).

The overall economy still looks like it’s in the midst of “the littlest recession” with indications it fading in JOLTS data while unemployment is lagging behind (as was seen with the 2008 recession).

Core unemployment rate is U3 minus temporary layoffs — as layoffs went haywire in the pandemic. Note this return to the pre-stimulus / post-pandemic dynamic equilibrium could also be happening in the headline unemployment rate (n.b. Goldman-Sachs: Nice On!):

Initial claims (ICSA) divided by the size of the civilian labor force (FRED CLF16OV).

Note that 0.15% ~ 1/√N where N = 500,000 is the typical scale of initial claims.

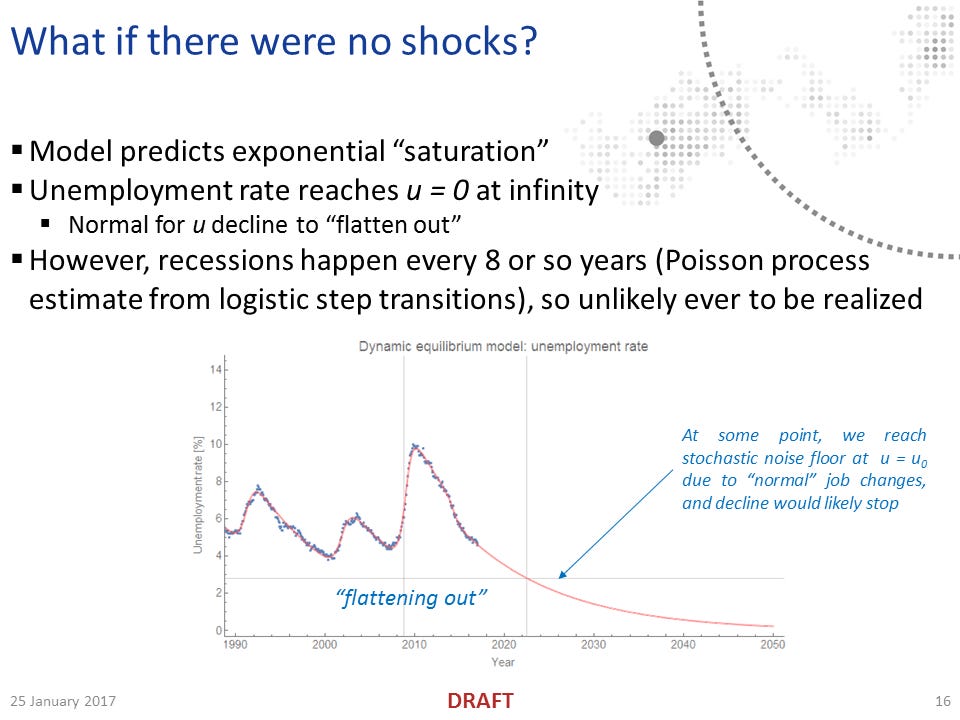

I noted this back in early 2017 when I first put the DIEM together. See also this presentation slide: