Zen kōan inflation targeting

Tyler Cowen suggests the rather silly "target 4% to achieve 2% inflation" monetary policy for the ECB. I'm not sure if he actually meant it as a joke or not, but it certainly illustrates the utter ridiculousness of model-independent expectations that aren't the constrained "rational expectations" typically used in economic models.

Rational expectations are perfectly fine: you have an underlying model and the economic agents expect e.g. the level of inflation predicted by the model. In some sense, rational expectations make the economic agents superfluous. If the agents are just going to parrot back the expected values of model random variables, why not just say they aren't there. A better word for "rational" expectations would be model-dependent expectations, which I contrast with model-independent (MI) expectations above. These MI expectations are those typically invoked by e.g. Scott Sumner and Nick Rowe.

Cowen suggests that the ECB could target 2x% in order to achieve x% inflation relying on MI expectations. With MI expectations however, if the ECB doesn't keep this a secret, the agents will learn 2x really means x, and then the 4% inflation target will really be a 1% inflation target since 4% means the ECB is aiming for 2% so will only achieve 1%. Okay, then.

But here's where it really gets silly. If you see the ECB's current 2% target as not credible, then aiming for 4% and resulting in 2% manufactures a credible 2% inflation target out of an incredible one by renaming "two" as "four". Incredible!

Another solution, proposed by Scott Sumner, is that the ECB doesn't actually want 2% inflation, even though it says it does, but rather the ECB communicates its inflation targets by talking about unemployment and competitiveness. Yes, the official inflation target is 2%, but that is irrelevant: the actual inflation target is 1% because that is what makes the PIIGS competitive.

[*slice*]

Yes, that was Occam's razor.

Sure, countries seem to be able to achieve their inflation targets most of the time (in fact, the quantity theory of money works for a lot of cases), but now we have a series of countries that seem to be undershooting them a bit: Japan, US, EU, Canada ... etc. Maybe there is a maximum achievable inflation rate i* for an economy? For countries with inflation targets below this maximum, inflation targeting works: the central bank says 2%, it gets 2%. For countries with inflation targets above this level, all you get is the maximum i*.

The information transfer model produces this result. At every point on the price level surface (see e.g. here, or at the top right of this blog if you're not viewing it on a mobile device), there is a maximum gradient (inflation rate). This is the inflation limit at that point. During the 1960s in the US, this maximum inflation rate was 10% or more.

EU i* is predicted to be low by this model (almost zero) -- below their target of 2%. For the US, i* is just below 2%.

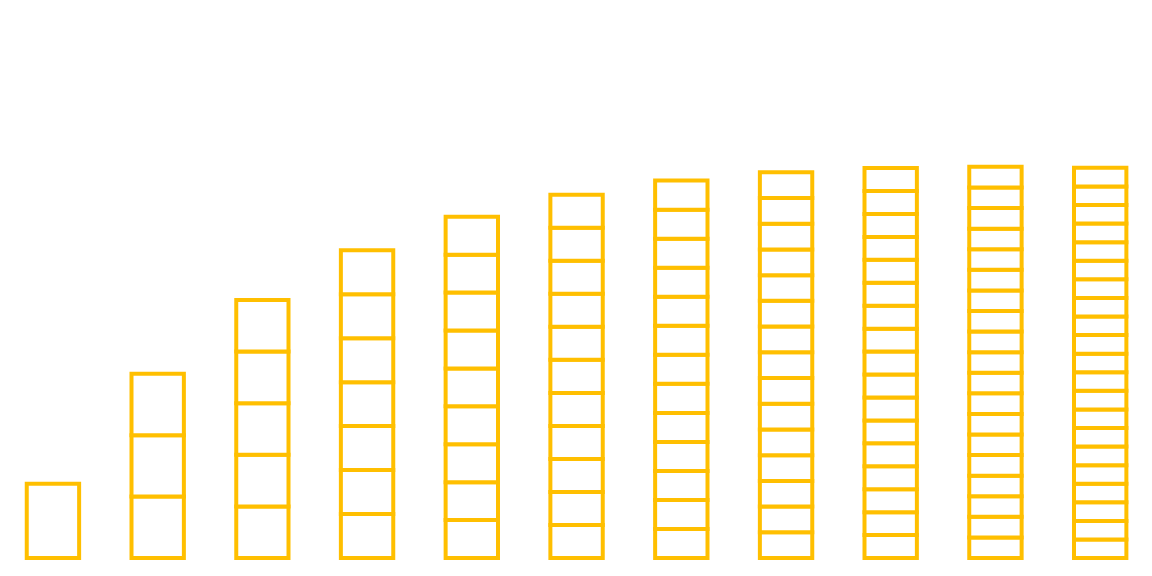

Where does this maximum come from? Money has two purposes: it is the medium of exchange, allowing transactions to occur and it is the unit of account, Fisher's measuring stick. In the information transfer model, money allows people to exchange information and measure the units of the information. As you increase the amount of money, the relative impact of these different capacities changes. You can imagine the unit of account as a box that gets smaller as more money is added to the system, while the medium of exchange is the number of boxes. The height of that stack is proportional to the price level. And it looks something like this:

Japan is on the right side of this diagram, while, say, China in on the left. The maximum inflation rate i* is the slope, higher on the left and lower on the right.

This is Cowen's "most economical model".