New CPI data, and an IE model gets rejected

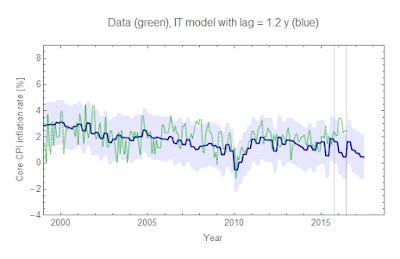

There is new CPI data out today, so I've updated the lag model. It looks like it's not doing too well. There's the spike in January/February, which might be transient. It's within 3 sigma (0.03%, or one month in 30 years), but it occurs in both PCE and CPI data which makes it more like 4.5 sigma (one month in 12,000 years -- since the last ice age). That's troubling, but another problem is the IE lag model is consistently under-estimating the last 8 measurements of CPI inflation (there's a bias), which is a 0.4% probability event (about 3 sigma) on its own.

I could try to console myself with the fact that the measurement of CPI inflation changed slightly in January 2016 (they started using an arithmetic mean for prescription drug prices, but that's a small component of CPI). However that doesn't fix the consistent bias. I'll still follow this model however -- the data does show periods of persistent over- and under- shooting.

Note that this is just the lagged-GDP model of CPI inflation (that I'd hoped might squeeze a few basis points more accuracy out of the data), not the PCE inflation model that is in a head-to-head competition with NY Fed DSGE model (see here for the list of predictions).